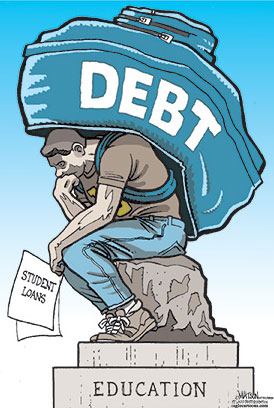

student loan consolidation is one of the most commonly used methods for reducing and working with student debt. If you want to consolidate debt, whether the student loan debt or not, you have to follow a specific process. However, this process is easy to follow and will absolutely not require big efforts from your side.

Here is what you need to know about the consolidation process: You combine all your different student loans into one big loan. Instead of paying toward all your loans each month, you can make one payment towards this one loan. So, what do I get to that, May you ask. If you compare the numbers before and after you have consolidated your student debt, you will realize that this is a very good job.

to begin a career working with a lot of the debt is a daunting prospect to say the least. But the fact is that many college graduates unfortunately are facing this situation. Fortunately consolidating your student loans is a great way to meet the challenge of getting rid of the burden of debt from school or college.

The main benefit of consolidation is that you generally pay a lower interest rate then compared to what your various loans are already set to. It works the same way as refinancing a home to a lower mortgage payment. And be aware that the current interest rate was the lowest in almost 40 years. When you do this consolidation will pay an interest rate, not several different rates. And at a time when these loans, the prices are probably higher.

, which means money saved: lower interest rates on a relatively big loan can save you thousands of dollars in the long run. And besides, some lending companies offer rate reductions for students consolidating their loans while they are in their počeka.Upozorenje to: Stay away from companies that require you to start immediately after the payment grace period. There are financing companies out there that do not require. Go to them !!!

And if that was not enough, some companies even offer additional rate reductions. I've heard about companies that reduce the rate of one per cent if you make all your payments on time for two years. And it comes with the discounts described above. One percent of May seem small, but if you see it in perspective, let's say 20 years, the normal payback schedule, it can mean lots of dollars saved.

Another advantage of the student debt consolidation is saving time and effort. It is much easier to handle one payment monthly than several separate payments.

convenient way to do this monthly payment is to let the loan company deduct it directly from your bank account. Some companies allow. And if it is really a good student loan consolidation, even though it will give you a slight decrease of interest in handling your loan payments so the rate.

So, if you find that loan consolidation is (in) for you, your challenge is to decide which business loan consolidation approach and ultimately select. What I recommend is to make a list of questions you might have, call several companies and speak with their representatives. Or you can go online to find a good student loan consolidation companies. There are some great companies out there.